#2: What Do We See?

When it comes to climate and finance, we know enough to predict a few things with confidence. It requires attention. Paying attention involves seeing things differently.

PRESSED FOR TIME?

Capital markets are about the movement of money. Money typically moves towards safety and away from risk. From this basic principle, we know quite a lot about how efficient financial markets will respond to climate change.

Understanding this financial principle is important, but understanding the visual prompts for how things are changing around us is even more critical. We aren’t ever taught to observe slow onset change in the world around us, but this skill is pivotal in realising how the story of money, risk and a changing climate will weave together.

HOW TO SEE

In his seminal 1977 design work How To See, George Nelson showed humans are never taught ‘visual literacy’, or the ability to recognise, evaluate, and understand the objects and landscape of the man-made world.

A simple example is the idea of visual pollution: we walk past a disorganised pole wire and something deep in us reacts negatively to it, though we don’t have a vocabulary to describe why we don’t like it. In contrast, the symmetry of a tree in nature is restful and reassuring. We have always been in search of order.

This newsletter issue is about how a changing climate costs money, and why someone always has to pay. But the journey to understanding that topic involves revisiting how we see things everyday, and the ways a changing climate affects the world around us.

HOW EVERYTHING CHANGES

As we touched on in our opening welcome, climate change is everything change.

It is already impacting or is anticipated to impact nearly every facet of the economy. Here are a few examples to think about:

INFRASTRUCTURE: A dirty secret our politicians are never honest about is our infrastructure is decaying from the moment we erect it. There is always more to spend because everything is on a journey to obsolescence.

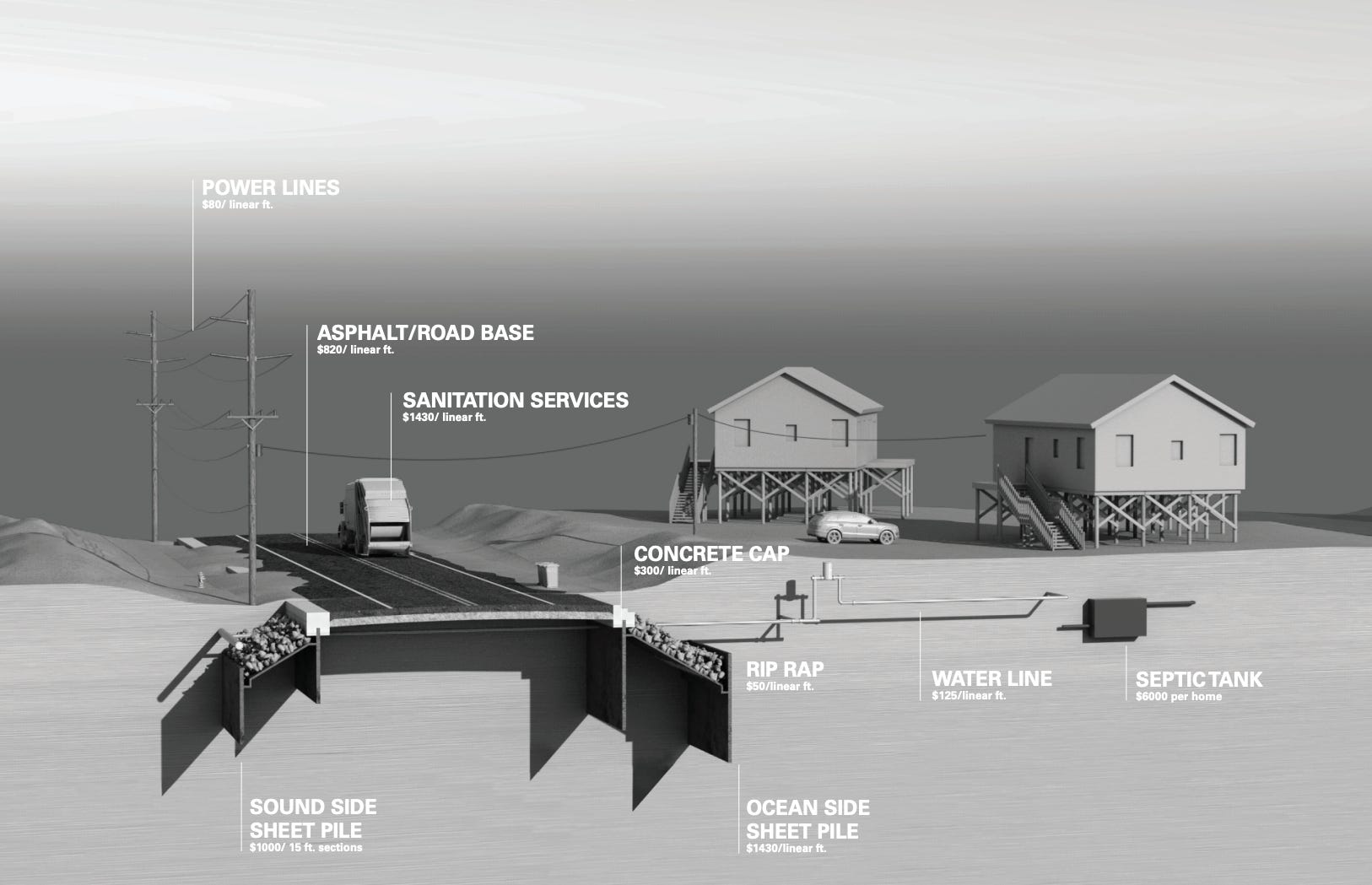

Research (above) has shown the cost of repairing roads on a North Carolina barrier island after a storm already outweighs the economic logic of the property tax base and the sparse population that lives there. This is happening the world over, where we’ve built roads, power lines and other amenities in places where not a lot of people live and have jobs. Each time a disaster hits, the number of people who can shoulder the cost for the repairs is disproportionate to the ever-rising cost. This poses difficult questions for the services provided to remote communities who live in vulnerable climate settings

Question: Have you ever stopped to look at the infrastructure on your street, in your neighbourhood, on the road to work or your nearest holiday destination? Have the cables been sunk to improve the view? Are cracked pavements repaired? Do residents routinely tend to their gardens? Does someone come to mow the lawn on an empty plot? All of these small prompts make up little hints of the urban experience: they tell us where there is money, jobs, growth and often, a willingness to pay for long term risk mitigation.

AGRICULTURE: The major food baskets of the world all see their crop yields fall with even small rises in global average temperatures. In one year, planted acres of rice in Matagorda County, Texas, dropped from 22,000 acres to 2,100 acres (Baddour, 2014). The effects didn’t stop at a poor crop: the ripple effect on the local economy in that case study was severe, with a 70% decline in sales of farm implements and machinery. Some family-owned establishments that had survived for decades closed permanently.

Feeding a growing global population in a changing climate presents a significant challenge, with winners, losers, logistics shifts and changing consumption habits. It also poses challenges for parts of the world where most of the economic value is found in just a few vulnerable sectors

Question: Leave any guilt about carbon footprints at the door for now, let’s just give thought to the scale and economic forces at work. Do you look to see where your food in the grocery store is grown or made? Does it have a short shelf life, and if so, do you ever count the driving or flight days it maybe took to reach you? Do you tend to eat a lot of almonds (a water-intensive, non-essential farmland product) or corn, soybeans and rice? London strawberries might come from Egypt or Morocco, while Boston blackberries might come from Mexico. If you eat a banana anywhere on earth, there’s a 30% chance it came from Ecuador. Thinking about climate change in places you don’t live takes on a new dimension when you stand in front of your kitchen fridge or pantry cupboard.

PROPERTY: Nearly everything about where we live and what it costs will change. E.g. this visual shows a stretch of the Alabama coastline where oceanfront development lots were taken by the sea years ago, but still are in the property tax system (NB: The white line that moves unevenly along the lower edge of the picture is where the shoreline used to be when the development was zoned for sale).

This problem is not confined to the waterfront and sea level rise, because the conditions around a lot of real estate near rivers or other low-lying wetlands or lake areas have also changed. Wildfires are arguably no different: when people live on the edge of a large national forest, capable of high wind fires that move faster than our speed of response, a risk isn’t priced into what people have paid for that asset. It mean assets can’t be insured the same way, or don’t find a liquid market of buyers because of their location when someone goes to sell it (NB: I will spend future newsletters talking about this in much greater detail).

Question: Where is the nearest waterfront — ocean, river, lake or wetland — to your home? What happens to your green areas after a large storm? Does water sit for periods? What has been happening to your insurance policy over the last decade? What about your holiday home if you own one? What was the hottest day in your town last year, and how did this compare to the frequency of very hot days when you were a kid? How seriously does your local government take storm and fire management? Because most of us have a large portion of our net worth tied up in the family home, this is an area we all need to pay greater attention.

HEALTH: Air pollution kills an estimated seven million people worldwide every year (for perspective, this is 7x the global coronavirus death toll from 2020, but every year). WHO data shows that 9 out of 10 people breathe air that exceeds WHO guideline limits containing high levels of pollutants.

Everyday air quality isn’t linked to climate change in most people’s minds like a hurricane or melting iceberg, but we’re effectively developing a dangerous cocktail for the human body in the world’s major cities: (i) poor air to breathe; and (ii) average temperatures that on extreme heat days, become dangerous to be outside — not just construction workers or same-day delivery drivers, but children or the elderly being outdoors in direct sunlight for more than an hour.

Extreme heat will become a much bigger part of our global story. In the 1920s Phoenix averaged about 75 days that registered 38°C (100°F), roughly 20% of the year. Between 1980 and 2010 the average was 110 such days, 30% of the year. in 2020 there were 145, 40% of the year. At what point does it become too difficult to be outside?

Question: What temperature do you now start to feel uncomfortable in summer? How do your habits, activities and choices change if you see the temperature forecast is 35°C (95°F)..? Can you see a clear line of smog over the city skyline on some days of the year when you commute into work? If so, how often?

SEEING A CHANGING CLIMATE WITH MONEY IN MIND

To now, financial markets have simply left a changing climate outside of much of their modelling and forecasting: it’s too big, and with too many variables. That will change.

We will delve far deeper into all these topics in coming issues: the places where the risk is appearing first, the companies offering solutions, the attitudes and early price signals the market is giving us.

But this is the most important idea to understand early..

EVERYTHING ADVERSE THAT HAPPENS IN OUR ECONOMY, SOMEONE HAS TO PAY.

HERE’S WHAT WE KNOW

For every action in the economy, there is someone willing to take a risk for a given return, and someone willing (or not willing) to lend against that risk. When crops fail, or roads crack, or house prices lose value in a flood, there is someone holding a loss. Someone always has to pay.

Here’s another problem. While an understanding of particular kinds of climate risk is advancing quickly, understanding about how different types of climate risk will interact with each other remains in the earliest stages. Climate models are good, but financial models that try to model Value at Risk (VaR) or expected shortfall are not at the same level — yet. We will delve more deeply into this too.

CONCLUSION (FOR NOW)

A lot of change is already underway.

We can confidently predict the following:

more regulations on how companies and people pollute, the materials they use in everyday life, and what is built

new financial disclosure laws forcing companies to understand their supply chain in the context of emissions

higher insurance premiums for businesses and homeowners, and

difficult fights over property tax rates to pay for a built environment that is expensive to refit and repair.

In the coming issues we will explore many more specific questions, but as an opening idea, we need to be aware climate change will not always be something we’re trained to observe. Not every cracked pavement, hail storm or crop season is new and completely related to the climate, but the climate does play into how we’ve typically understood all the costs around us.

We need to think not only about what we’re seeing, but how we’re seeing. As George Nelson showed, no one is really taught how to see. Once we start to see signals, we also need to continually ask: who pays, when, and do they realise it yet?

Let’s try and uncover those hidden stories of a changing climate together.

Optimistically,

Owen C. Woolcock

3 Questions I Am Asking Myself This Week

1. With the Biden Administration now recommitted to the Paris Agreement, how will Big Business use the time between now and Glasgow (COP26) in November? Which companies will make pledges independent of nations, and what kind of novelty or original thinking might be in those commitments?

2. If Phoenix experience 145 days in 2020 at or above 38°C (100°F), how many would it take for the inbound retiree waves to course-correct? Could it be happening now and we’ve not yet seen it in the data?

3. If I was an investor in a luxury hotel on the waterfront of a remote Pacific Island, how would I be thinking about managing that risk?

If You Read Or Listen To One Thing This Week

Politico, How Climate Change Could Spark the Next Mortgage Disaster (Oct. 2020): A well-written article on the looming home ownership crisis that many experts have discussed, but is difficult to reform with so many institutional interests.

References

Stein, I., Elkin, R., Stang, M., & Harvard University. Graduate School of Design. (2019). Lines in the Sand : Rethinking Private Property on Barrier Islands.

Challinor A. J., Watson, J., Lobell, D. B., Howden, S. M., Smith, D. R., & Chhetri, N. (2014). A meta-analysis of crop yield under climate change and adaptation. Nature Climate Change, 4(4), 287-291

Baddour, D. (2014, 8th December). During Drought, Once-Mighty Texas Rice Belt Fades Away. Texas NPR, retrieved from https://stateimpact.npr.org/texas/2014/08/12/during-drought-once-mighty-texas-rice-belt-fades-away/